Field Note

What Is a PCI Non-Compliance Fee?

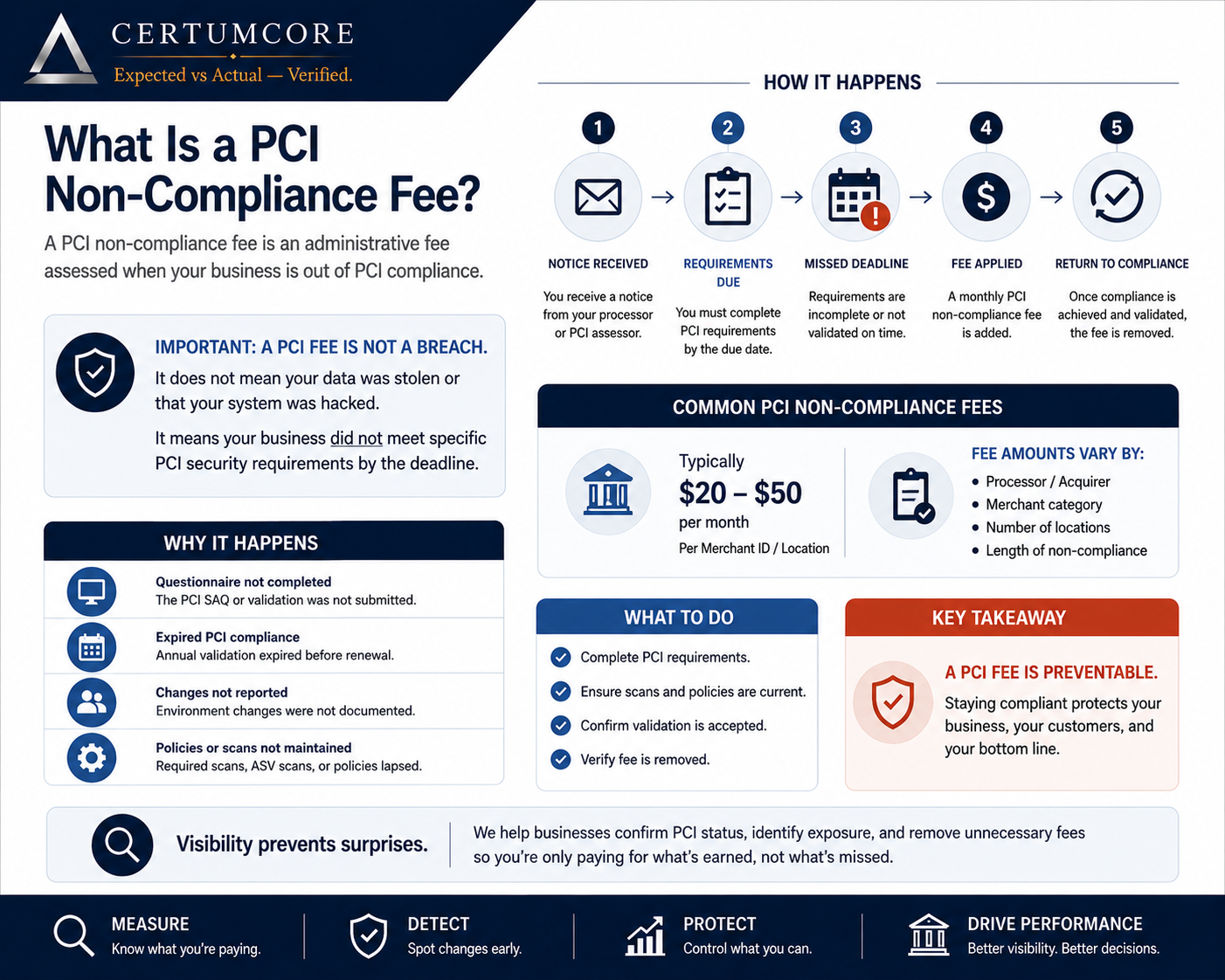

A PCI non-compliance fee is usually a processor charge tied to payment-security validation, documentation, questionnaires, or missing compliance evidence.

The fee does not automatically mean a breach occurred. It does mean the business should understand what the processor is charging for and what evidence is missing.

Expected vs Actual — Verified.

What is a PCI non-compliance fee?

A PCI non-compliance fee is a charge that may appear on a merchant processor statement when a business has not completed or maintained a required payment-security validation step.

That may involve a PCI questionnaire, validation status, documentation requirement, processor notice, scan requirement, device environment question, or other payment-security-related workflow.

A PCI fee does not automatically prove the business is unsafe.

It also does not automatically mean the fee should be ignored. The fee is a signal that the business should understand what the processor expected, what was submitted, and what remains unresolved.

PCI Non-Compliance Fee Signal

A PCI fee is not automatically a breach. It is a signal that payment-security evidence or validation may need review.

Why PCI fees confuse businesses

PCI-related fees are confusing because they often show up as processor statement line items without enough plain-language explanation.

A business owner may see wording such as:

- PCI non-compliance fee

- PCI fee

- compliance fee

- monthly security fee

- data security fee

- SAQ-related notice

- scan or validation notice

Sometimes the business completed something but the processor record does not reflect it. Sometimes the business completed the wrong questionnaire. Sometimes the business never saw the notice clearly. Sometimes the fee keeps billing because nobody follows up.

The issue is not only the fee. The issue is the uncertainty around why the fee exists.

Does a PCI non-compliance fee mean there was a breach?

Not necessarily.

A PCI non-compliance fee does not automatically mean card data was breached, stolen, or exposed. It may simply mean the processor does not have the required validation evidence on file.

But a business should still take the signal seriously because PCI questions are connected to how payment card data is handled, stored, transmitted, segmented, or protected.

The fee may be administrative. The underlying payment-security scope may still matter.

Common reasons a PCI fee appears

PCI-related fees may appear for several reasons.

- a questionnaire was not completed

- the wrong questionnaire was completed

- a required scan was not completed

- the processor did not record the submitted information

- business operations changed

- payment devices or workflows changed

- the business uses keyed or virtual terminal payments

- the business has multiple locations or systems

- the processor requires annual revalidation

None of these should be guessed at from the fee alone. The statement, processor notices, payment workflow, and actual business environment should be compared.

Why payment-security scope matters

Payment-security scope is about what systems, devices, people, networks, and workflows touch payment activity.

A simple card-present terminal may create one kind of scope. A virtual terminal, keyed-entry workflow, back-office payment screen, stored-payment process, or multi-location environment may create a different scope.

If the business answers processor questions based on assumptions instead of actual workflow, the result may not match reality.

PCI readiness is not only about checking a box. It is about whether the answers match the environment.

When should a business investigate a PCI fee?

A business should investigate PCI fees when the pattern is unclear or the charge keeps appearing.

Warning signs include:

- PCI fees appear unexpectedly

- PCI non-compliance fees repeat monthly

- the business believes it already completed the required step

- processor explanations are inconsistent

- payment devices or workflows changed

- keyed or virtual terminal payments are used

- multiple locations answer PCI questions differently

- the business does not know which systems are in payment scope

The goal is not alarm. The goal is to determine what the fee represents and whether the business has evidence to support its payment-security answers.

What CertumCore looks for

CertumCore reviews PCI fee signals as part of payment operations visibility and payment-security scope awareness.

CertumCore does not certify PCI compliance and does not provide legal advice.

The goal is to compare expected payment-security responsibilities against actual payment workflows, processor notices, statements, devices, and available records.

A review may look at:

- whether PCI-related fees appeared or changed

- whether the processor statement shows recurring compliance charges

- whether keyed or virtual terminal workflows affect scope

- whether payment devices and workflows match the business’s assumptions

- whether processor notices require follow-up

- whether multiple locations have inconsistent payment-security answers

The question is not only “why is there a fee?”

The better question is: “What does the fee reveal about the business’s payment environment?”

Related review

PCI Readiness Review

CertumCore reviews payment-security exposure, PCI scope, payment devices, segmentation, vendor responsibilities, and evidence readiness before processor questionnaires.

Request ReviewFrequently asked questions

What is a PCI non-compliance fee?

A PCI non-compliance fee is a processor charge that may appear when a business has not completed required payment-security validation, questionnaires, documentation, or related processor requirements.

Does a PCI non-compliance fee mean my business had a breach?

Not necessarily. A PCI non-compliance fee does not automatically mean a breach occurred. It may reflect missing validation, incomplete questionnaires, unclear scope, or processor-side documentation requirements.

When should a business investigate a PCI fee?

A business should investigate when PCI fees appear unexpectedly, repeat monthly, increase, conflict with processor explanations, or when the business does not understand its payment-security scope.