Field Note

How To Read A Merchant Processing Statement

A merchant processing statement shows how card payments were processed, deposited, adjusted, and charged during a billing period.

The statement is not just paperwork. It is one of the clearest records a business has for understanding payment cost, transaction behavior, settlement activity, and operational drift.

Expected vs Actual — Verified.

What is a merchant processing statement?

A merchant processing statement is a record from a payment processor showing card payment activity for a period. It usually includes sales volume, transaction counts, fees, deposits, refunds, chargebacks, adjustments, and processor charges.

Many businesses receive these statements every month but do not fully review them. That creates a visibility gap.

A business can receive deposits and still not understand whether the payment system behaved as expected.

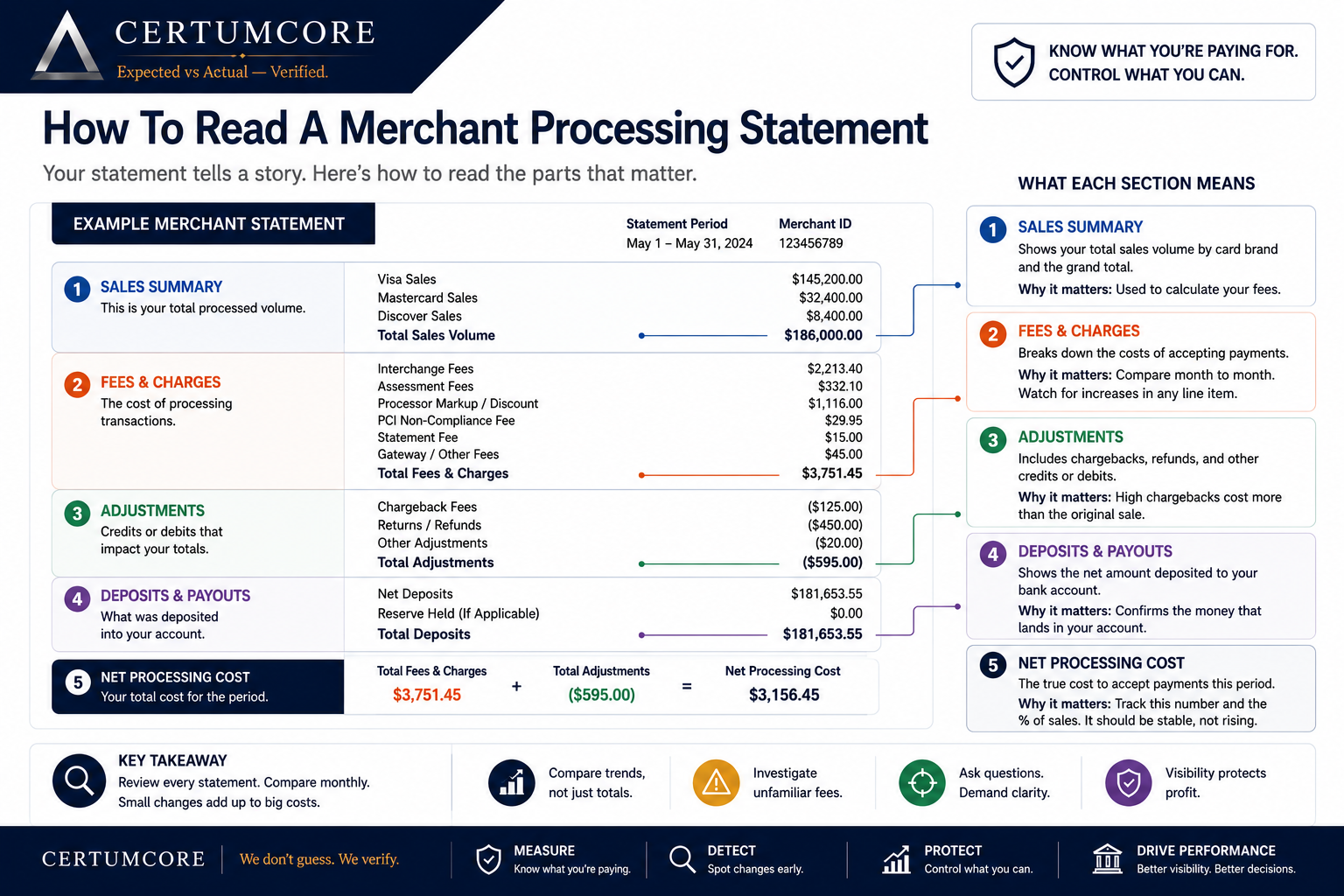

Merchant Processing Statement Map

A processor statement should be read by separating sales volume, fees, adjustments, deposits, and net processing cost.

Start with total processing volume

Processing volume shows how much card activity moved through the processor during the statement period. This may include card-present payments, keyed payments, online payments, invoice payments, refunds, or other transaction categories.

Processing volume should be compared against the business’s own expectations. If sales volume changed, fees may change too. But if fees rose faster than volume, the statement deserves closer review.

Do not stop at the total. The mix of transactions matters.

Compare deposits and settlement activity

Settlement activity shows how payment batches turned into deposits. A statement may show gross sales, refunds, chargebacks, fees, reserves, adjustments, and net deposits.

Business owners often focus on whether money reached the bank. That matters, but it is not the whole picture.

A useful review asks:

- Do deposits match expected batches?

- Are settlement delays normal for the processor?

- Are refunds, chargebacks, or adjustments reducing deposits?

- Are fees being deducted daily, monthly, or both?

- Are multiple locations settling differently?

Identify the fee categories

Merchant statements often combine several types of fees. The names vary by processor, but common categories include:

- interchange fees

- assessment or network fees

- processor markup

- monthly account fees

- statement fees

- batch fees

- gateway or software fees

- PCI-related fees

- chargeback fees

- adjustments or miscellaneous line items

Some fees are expected. Some may be new. Some may repeat without anyone noticing. The point is to separate what is normal from what changed.

Calculate the effective processing rate

The effective processing rate is a practical way to understand overall payment cost. It compares total processing fees against total processed volume for the period.

For example, if a business processed $50,000 and paid $1,500 in processing fees, the effective rate would be 3%.

The exact rate matters less than the trend. If the effective rate moves from one month to the next, the business should understand why.

Fee movement without explanation is the signal.

Look for keyed transaction activity

Keyed transactions happen when card information is manually entered instead of captured by tap, chip, or swipe.

Some keyed transactions are legitimate. Phone orders, virtual terminals, damaged cards, invoice payments, and back-office workflows may all create keyed activity.

But if keyed activity increases unexpectedly, the business should investigate. More keyed activity may affect cost, fraud exposure, chargeback risk, and processor classification.

Related Field Note

What Is a Keyed Transaction?

Learn why keyed transactions matter and when keyed activity should be treated as an operational signal.

Review PCI fees and payment-security notices

PCI-related fees may appear as compliance fees, non-compliance fees, data security fees, or processor notices.

A PCI fee does not automatically mean the business had a breach. It may mean a questionnaire, validation step, scan, or processor record is incomplete.

The key question is whether the business understands its actual payment-security scope and whether processor records match that reality.

Related Field Note

What Is a PCI Non-Compliance Fee?

Learn what PCI non-compliance fees may mean and when businesses should investigate them.

Watch for new or recurring adjustments

Adjustments can be easy to overlook because they may appear as small statement line items. But recurring adjustments, unexplained corrections, charge categories, or new fees can change the cost profile over time.

A single adjustment may be routine. A pattern of adjustments deserves review.

The statement should help answer:

- What adjustment occurred?

- Why did it occur?

- Did it happen before?

- Is it tied to refunds, disputes, pricing, processor correction, or transaction type?

- Does it repeat?

Compare this month against prior months

A single merchant statement gives a snapshot. Comparing statements over time gives a pattern.

Month-to-month comparison can reveal:

- effective rate movement

- new fees

- rising keyed transaction share

- PCI-related charges

- more frequent adjustments

- changes in settlement timing

- different behavior across locations

This is where fee drift becomes visible. The business may not notice a gradual change until the pattern is compared over time.

Common warning signs

A merchant statement deserves closer review when:

- fees rise faster than sales volume

- the effective processing rate increases

- new line items appear

- PCI fees appear or repeat

- keyed transactions increase

- chargebacks or disputes increase

- settlement deposits become harder to match

- processor explanations do not match the records

- different locations show different payment behavior

The question is not only whether the business paid more. The question is whether the statement explains why.

What CertumCore looks for

CertumCore reviews merchant processing statements to establish visibility into payment behavior, fee movement, keyed activity, settlement activity, PCI fee signals, and operational drift.

The goal is not alarm.

The goal is to compare expected payment behavior against actual payment behavior.

A review may look at:

- whether the effective processing rate changed

- whether new fees or adjustments appeared

- whether keyed transaction activity increased

- whether PCI-related fees require explanation

- whether deposits and settlements match expectations

- whether multiple locations behave consistently

- whether processor records support what the business believes is happening

A processor statement is not just a bill. It is evidence.

Related review

Processor Statement Review

CertumCore reviews statement fees, adjustments, PCI signals, settlement behavior, keyed transaction exposure, and effective cost movement.

Request ReviewFrequently asked questions

What is a merchant processing statement?

A merchant processing statement is a record from a payment processor showing payment volume, fees, deposits, chargebacks, adjustments, and other processor activity for a period.

What should I look for on a merchant processing statement?

Review sales volume, total fees, effective processing rate, interchange, assessments, processor markup, PCI fees, adjustments, chargebacks, refunds, settlement timing, and keyed transaction activity.

When should a merchant statement be reviewed?

A merchant statement should be reviewed when fees increase, new line items appear, keyed transactions increase, PCI fees appear, deposits are harder to reconcile, or processor explanations do not match the records.