Field Note

Why Do My Credit Card Processing Fees Keep Going Up?

Credit card processing fees may keep increasing even when nothing obvious appears to have changed.

The important question is not only whether fees went up. The better question is what changed, why it changed, and whether the statement evidence supports the explanation.

Expected vs Actual — Verified.

What business owners usually notice first

Most business owners do not start by noticing interchange, assessment fees, processor markup, or transaction classification. They usually notice something simpler.

- processing fees seem higher

- deposits seem smaller

- statements are harder to understand

- new fees appear

- support explanations feel unclear

- nothing obvious changed in the business

That last point is what makes the problem frustrating. The business may be operating the same way, but the cost profile may still move.

Fees can increase without the payment system completely failing.

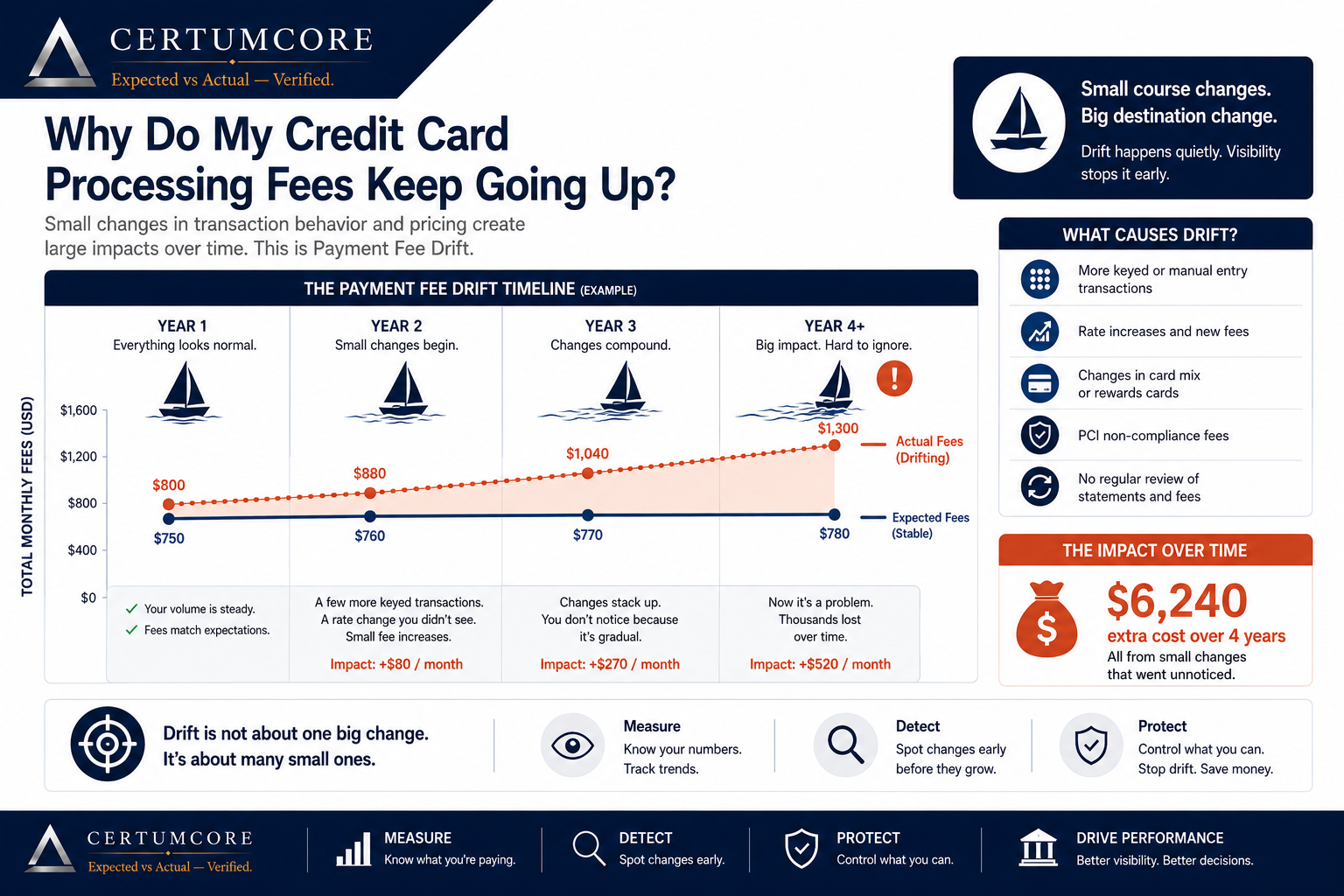

Payment Fee Drift Timeline

Payment Fee Drift is not usually one big change. It is often several small changes that compound over time.

Why processing fees may keep increasing

Credit card processing cost is usually made up of several layers. When one or more of those layers changes, the total cost can move.

Common causes include:

- interchange category changes

- assessment or network fee movement

- processor markup changes

- keyed or manual transaction increases

- PCI-related charges

- software or gateway fees

- new monthly recurring fees

- adjustments, chargebacks, or statement corrections

- changes in transaction mix

Not every increase means the processor is acting unfairly. But every unexplained increase deserves to be understood.

Interchange and assessments can affect the total

Interchange and assessment-related costs are part of the card payment system. The business may see their effect on the processor statement even if the processor did not create the entire increase directly.

Transaction type matters. A card-present tap or chip transaction may not carry the same cost profile as a keyed transaction, invoice payment, online payment, rewards card, or business card.

If customer payment behavior changes, the statement may change too.

Processor markup and recurring fees can grow quietly

Processor markup is the part of cost connected to the processor, platform, service provider, or pricing arrangement. It may include per-transaction fees, monthly fees, statement fees, batch fees, gateway fees, support fees, software fees, or miscellaneous line items.

Some of these fees are expected. The problem begins when new charges appear, recurring charges grow, or the business cannot tell whether the current charges match the original expectation.

A fee does not need to be hidden to become unclear.

Keyed transactions can change the cost profile

Keyed transactions happen when card information is manually entered instead of captured by tap, chip, or swipe.

Some keyed activity is normal. Phone orders, virtual terminals, damaged cards, invoice payments, and back-office workflows may all create keyed transactions.

But if keyed activity increases unexpectedly, processing costs, dispute exposure, fraud risk, and processor classification may change.

Related Field Note

What Is a Keyed Transaction?

Learn how keyed transactions work and when keyed activity should be treated as an operational signal.

PCI fees can add recurring cost

PCI-related fees may appear as compliance fees, non-compliance fees, data security fees, monthly security fees, or processor notices.

A PCI fee does not automatically mean the business had a breach. It may mean a questionnaire, validation step, scan, processor record, or payment-security scope issue needs attention.

If PCI fees repeat month after month, the business should understand why.

Related Field Note

What Is a PCI Non-Compliance Fee?

Learn what PCI non-compliance fees may mean and when businesses should investigate them.

Why businesses miss gradual fee increases

Gradual fee movement is easy to miss because the payment system often continues working.

- payments still process

- deposits still arrive

- monthly changes may look small

- statements are difficult to read

- nobody compares the same metrics month to month

- processor support may explain one fee without explaining the pattern

This is how small changes become normal. By the time the business notices, the pattern may have been present for months.

CertumCore calls this Payment Fee Drift

CertumCore uses the term Payment Fee Drift to describe gradual payment-cost changes that occur over time and often go unnoticed until they become meaningful.

Payment Fee Drift does not mean every fee is wrong. It means the cost profile moved away from what the business expected, and the reason should be verified with records.

A simple example:

| Month | Processing Volume | Processing Fees | Effective Rate |

|---|---|---|---|

| January | $50,000 | $1,250 | 2.50% |

| June | $50,000 | $1,500 | 3.00% |

In this example, the business processed the same volume, but total fees increased. That does not prove wrongdoing. It does prove the business should ask what changed.

Same volume. Higher cost. That is the signal.

Common signs of Payment Fee Drift

A business may be experiencing fee drift when:

- effective processing rate increases

- new recurring fees appear

- keyed transaction activity grows

- PCI charges appear or repeat

- statement complexity increases

- unexplained adjustments become common

- processor explanations do not match the statement

- one location becomes more expensive than another

- deposits arrive, but the cost profile changes

The issue is not always one dramatic event. Sometimes the issue is a pattern that was never reviewed.

How businesses can detect fee drift

A business can begin by comparing the same payment signals over time.

- compare processor statements month to month

- calculate effective processing rate

- review new and recurring fees

- track keyed transaction activity

- review PCI-related charges

- compare settlements and deposits

- look for adjustments, refunds, and chargebacks

- compare locations if the business has more than one

The goal is not to accuse the processor. The goal is to establish a verified baseline and identify whether the current payment behavior still matches expectations.

Related Field Note

How To Read A Merchant Processing Statement

Learn what to review on a processor statement and how to separate volume, deposits, fees, adjustments, and transaction behavior.

What CertumCore looks for

CertumCore reviews processor statements, fee movement, keyed activity, PCI fee signals, settlement behavior, and operational payment drift.

The goal is not alarm.

The goal is to compare expected payment behavior against actual payment behavior.

A review may look at:

- whether the effective processing rate changed

- whether new fees or recurring charges appeared

- whether keyed transaction activity increased

- whether PCI-related fees require explanation

- whether settlements and deposits match expectations

- whether processor records support what the business believes is happening

Higher fees are not always the problem. Unexplained fee movement is the signal.

Related review

Payment Fee Drift Review

CertumCore reviews processor records and fee movement to help businesses understand whether payment cost has changed and why.

Request ReviewFrequently asked questions

Why do my credit card processing fees keep going up?

Processing fees may keep going up because of interchange changes, assessment fees, processor markup, PCI fees, keyed transactions, software fees, gateway fees, new recurring charges, or gradual payment fee drift.

What is payment fee drift?

Payment Fee Drift is CertumCore's term for gradual payment-cost changes that occur over time and often go unnoticed until the business compares records and sees a meaningful change.

When should a business investigate rising processing fees?

A business should investigate when effective rate increases, new recurring fees appear, keyed activity grows, PCI charges appear, adjustments become common, or processor explanations do not match the statement.